Earnings season’s not over but — and the image on shopper spending is blended to this point.

The cost networks and banks have famous that although shoppers nonetheless are utilizing their playing cards, there have been some pullbacks by lower-income households. The Federal Reserve’s newest survey on shopper credit score detailed that use of revolving debt — which incorporates bank cards — slowed to an annualized tempo of 0.1% in March, down from a greater than 9% charge within the earlier month.

Spending might be and sometimes is lumpy, and the entire first quarter revolving debt grew at 5.7%. However that’s decrease than the 7.5% charge within the fourth quarter of 2023, and considerably under the year-over-year 9.7% charge that had been calculated a yr in the past.

For purchase now, pay later (BNPL) suppliers, pockets of serious progress are displaying by means of, lifting the fortunes of publicly-traded corporations, and offering proof — dovetailing with PYMNTS Intelligence’s personal knowledge — of acceleration in key classes similar to clothes and journey.

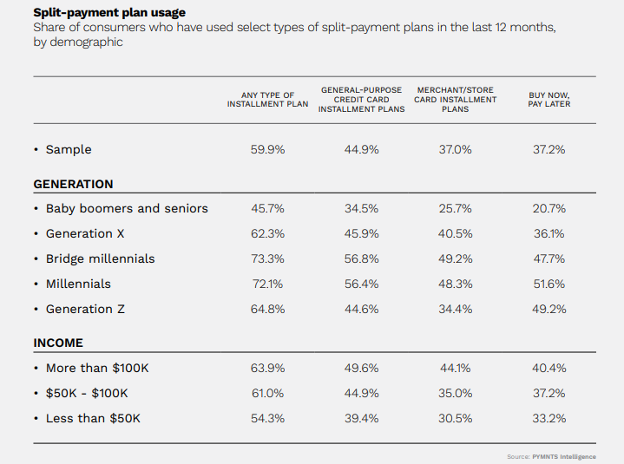

Coming into earnings, PYMNTS Intelligence, in collaboration with Splitit, discovered that three in 5 shoppers stated they’d used some split-payment choice at the least as soon as within the final yr.

Getting a bit extra granular, the surveys point out that 37% of shoppers had used BNPL. Greater than a 3rd of the bottom revenue shoppers had opted for BNPL, a share that will increase the upper up the revenue bracket one goes.

Those that tried it, favored it. PYMNTS Intelligence/Splitit discovered {that a} full 79% of shoppers had a positive expertise with the product.

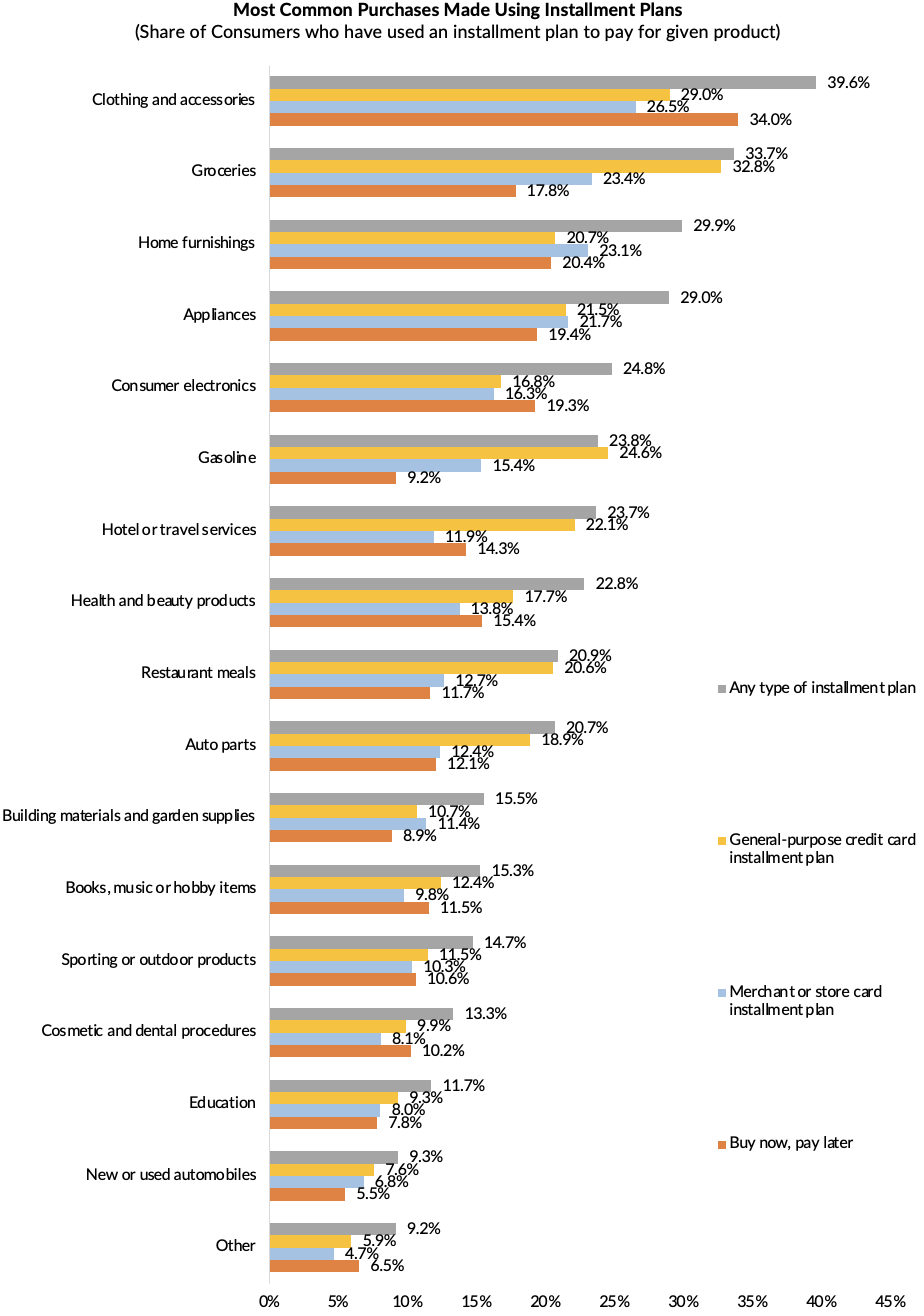

As to what they’ve been shopping for, the chart under signifies that of the shoppers utilizing installment plans, greater than a 3rd had used BNPL to purchase garments and equipment, 18% had performed so with groceries and greater than 14% had chosen BNPL when paying for travel-related providers.

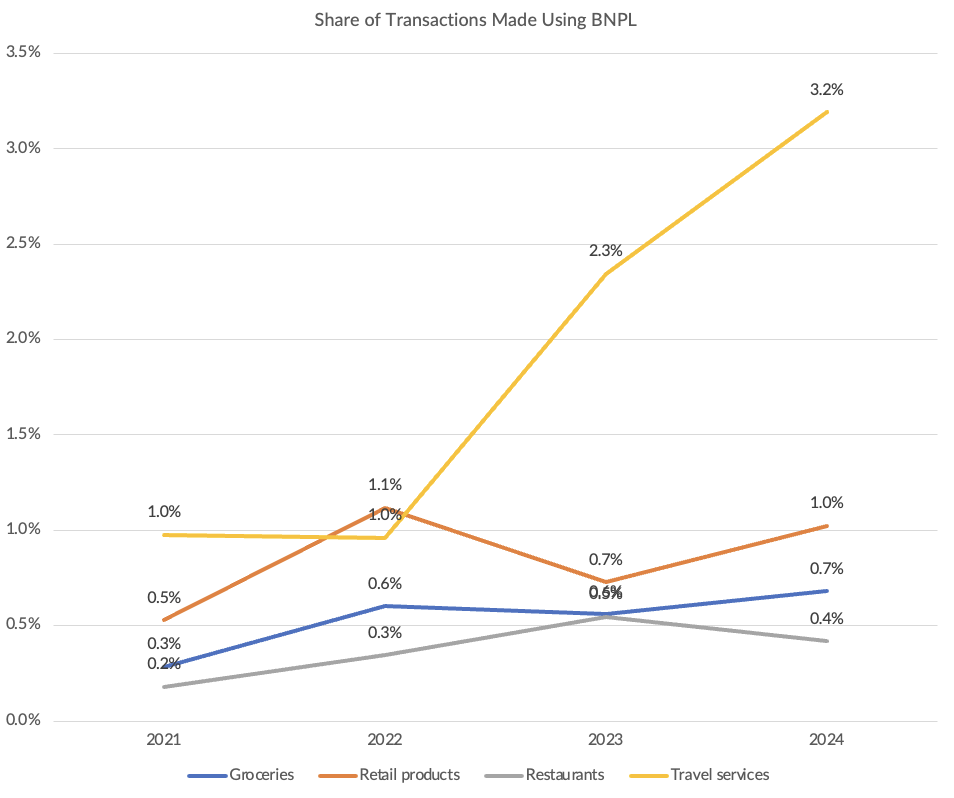

In accordance with the chart under, which makes use of knowledge from this spring primarily based on surveys with about 2,000 shoppers throughout three key classes, greater than 3% of shoppers had used BNPL to pay for journey as their most up-to-date transaction, and a a lot smaller proportion had performed so within the different classes. The runway, then, is lengthy for BNPL adoption.

Earnings Development

Earnings season corroborates the gathering momentum.

In Block’s first quarter report, administration famous that BNPL gross merchandise worth (GMV) was $6.98 billion within the first quarter, up 25% yr over yr.

And individually, on Wednesday (Might 8), Affirm’s fiscal third quarter outcomes disclosed 51% progress in revenues to $576 million, in addition to 4.7 transactions per common person (up 25% yr on yr), which signifies stickiness with the put in base. Affirm additionally offers a quarterly replace on spending classes. Within the newest studying, spending usually merchandise surged 49%, trend and sweetness was up 17% and journey/ticketing grew by 35%.

Sezzle’s report, simply out after the bell on Wednesday, stated that whole revenue was up 35%. The corporate stated in its earnings launch that underlying service provider gross sales rose by 33.2% to $492.7 million yr on yr, whereas shopper buy frequency elevated to 4.5 instances within the newest quarter, up from 3.1 final yr.

Within the present setting, excessive rates of interest on playing cards and the aforementioned slowdown in “conventional” revolving credit score debt could also be additional grist for BNPL adoption.

Coming into the tip of 2023, a couple of third of shoppers dwelling paycheck to paycheck stated they’d used BNPL, in response to PYMNTS Intelligence. Moreover, 30% of survey respondents indicated that the low or nonexistent rates of interest contributed to their resolution to use for BNPL. Roughly 19.4% valued the truth that the BNPL choices didn’t require a tough credit score verify. For 10% of the BNPL-using inhabitants, shoppers stated they’d not be capable to cowl payments had been BNPL not on provide.